import numpy as np

from scipy.stats import binom

import pandas as pd

from scipy.stats import norm

from statsmodels.formula.api import ols

import matplotlib.pyplot as plt第5章のPythonコード

第5章 推測統計の基礎

モジュールのインポート

5.1 統計的仮説検定の考え方

5.1.3 コイン投げの例

p40 = binom.cdf(k = 40, n = 100, p = 0.5)

p60 = binom.cdf(k = 60, n = 100, p = 0.5)

print(p60 - p40)0.95395593307065735.2 平均値の検定

5.2.5 Rによる例題演習

simdata = pd.read_csv('distributions.csv')

sample_mean = simdata.mean(numeric_only = True)[0]

sample_var = simdata.var(numeric_only = True)[0]

print(

"Mean of A: ", sample_mean, "\n",

"Varicane of A: ", sample_var, "\n",

"t-value: ", (100 ** 0.5) * (sample_var ** -0.5) * (sample_mean)

)Mean of A: 2.0423230835000004

Varicane of A: 0.37278460765476673

t-value: 33.449949007060785.2.6 \(p\)値

1 - norm.cdf(x = 1.250113) + norm.cdf(x = -1.250113)0.211258271555670785.3 回帰係数の検定

5.3.2 \(\hat{\beta}_1\)の分布のシミュレーション

np.random.seed(2022)

X = np.random.normal(loc = 0, scale = 1, size = 1000)

Y = 1 + 5 * X + np.random.normal(loc = 0, scale = 1, size = 1000)

mydata = pd.DataFrame(np.array([X, Y]).transpose(), columns = ['X', 'Y'])

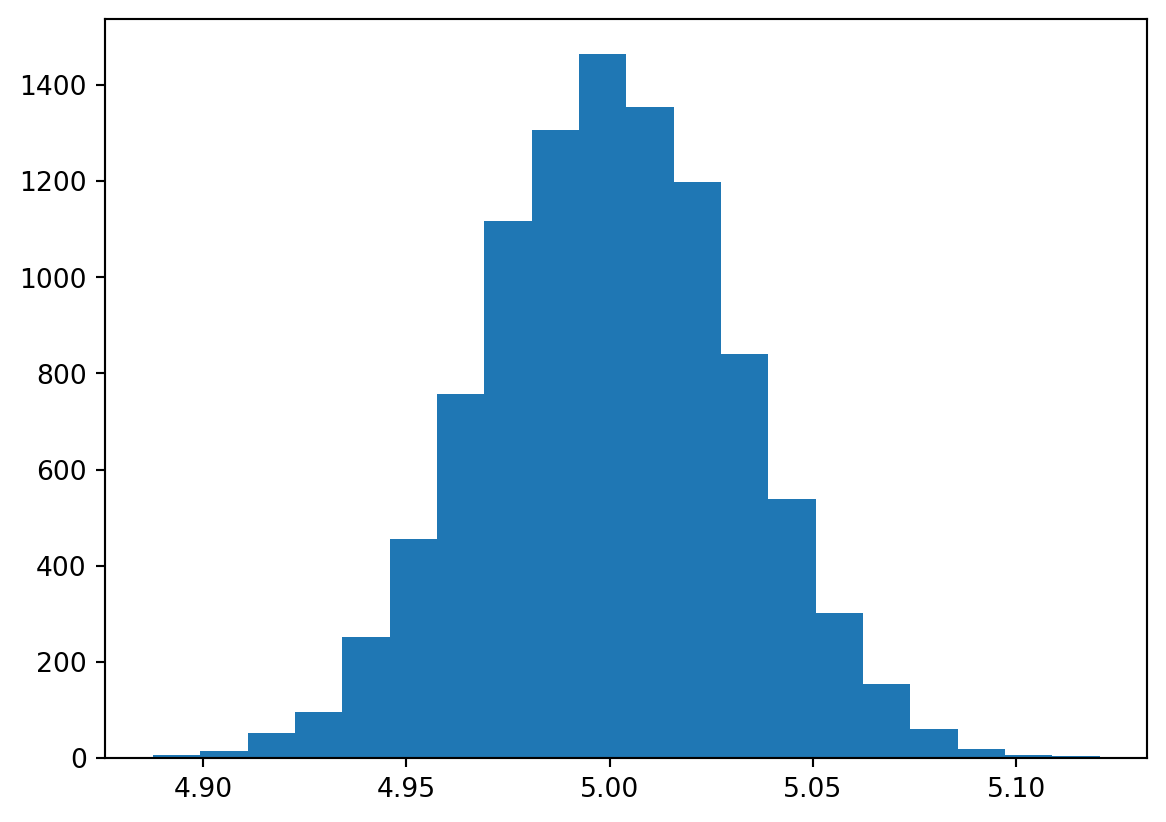

beta1 = ols('Y ~ X', data = mydata).fit().params[1]S = 10000

beta1 = np.zeros(S) # 結果の保存

for i in range(S): # 繰り返し開始

X = np.random.normal(loc = 0, scale = 1, size = 1000)

Y = 1 + 5 * X + np.random.normal(loc = 0, scale = 1, size = 1000)

mydata = pd.DataFrame(np.array([X, Y]).transpose(), columns = ['X', 'Y'])

beta1[i] = ols('Y ~ X', data = mydata).fit().params[1]

# 繰り返し終了pd.DataFrame(beta1).describe()| 0 | |

|---|---|

| count | 10000.000000 |

| mean | 5.000060 |

| std | 0.031486 |

| min | 4.887715 |

| 25% | 4.978288 |

| 50% | 4.999855 |

| 75% | 5.021525 |

| max | 5.120464 |

plt.hist(beta1, bins = 20)

plt.show()

5.3.6 Rによる分析例

wagedata = pd.read_csv('wage.csv')

wagedata['log_wage'] = np.log(wagedata['wage'])

result = ols('log_wage ~ educ + exper', data = wagedata).fit()

print(result.summary()) OLS Regression Results

==============================================================================

Dep. Variable: log_wage R-squared: 0.181

Model: OLS Adj. R-squared: 0.181

Method: Least Squares F-statistic: 333.0

Date: Wed, 05 Jun 2024 Prob (F-statistic): 2.32e-131

Time: 18:21:20 Log-Likelihood: -1524.1

No. Observations: 3010 AIC: 3054.

Df Residuals: 3007 BIC: 3072.

Df Model: 2

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 4.6660 0.064 73.147 0.000 4.541 4.791

educ 0.0932 0.004 25.796 0.000 0.086 0.100

exper 0.0407 0.002 17.417 0.000 0.036 0.045

==============================================================================

Omnibus: 37.191 Durbin-Watson: 1.739

Prob(Omnibus): 0.000 Jarque-Bera (JB): 41.243

Skew: -0.228 Prob(JB): 1.11e-09

Kurtosis: 3.348 Cond. No. 140.

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.print(0.0932 / 0.004)23.35.4 信頼区間

5.4.2 Rによる分析例

result = ols('log_wage ~ educ + exper', data = wagedata).fit()

print(result.summary()) OLS Regression Results

==============================================================================

Dep. Variable: log_wage R-squared: 0.181

Model: OLS Adj. R-squared: 0.181

Method: Least Squares F-statistic: 333.0

Date: Wed, 05 Jun 2024 Prob (F-statistic): 2.32e-131

Time: 18:21:20 Log-Likelihood: -1524.1

No. Observations: 3010 AIC: 3054.

Df Residuals: 3007 BIC: 3072.

Df Model: 2

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 4.6660 0.064 73.147 0.000 4.541 4.791

educ 0.0932 0.004 25.796 0.000 0.086 0.100

exper 0.0407 0.002 17.417 0.000 0.036 0.045

==============================================================================

Omnibus: 37.191 Durbin-Watson: 1.739

Prob(Omnibus): 0.000 Jarque-Bera (JB): 41.243

Skew: -0.228 Prob(JB): 1.11e-09

Kurtosis: 3.348 Cond. No. 140.

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.betahat = result.params

sigma = result.bse

lower = betahat - 1.96 * sigma

upper = betahat + 1.96 * sigma

pd.concat([lower, upper], axis = 1)| 0 | 1 | |

|---|---|---|

| Intercept | 4.541006 | 4.791063 |

| educ | 0.086089 | 0.100247 |

| exper | 0.036082 | 0.045233 |

result.conf_int(alpha = 0.05)| 0 | 1 | |

|---|---|---|

| Intercept | 4.540958 | 4.791111 |

| educ | 0.086086 | 0.100250 |

| exper | 0.036080 | 0.045235 |

result.conf_int(alpha = 0.01)| 0 | 1 | |

|---|---|---|

| Intercept | 4.501618 | 4.830451 |

| educ | 0.083859 | 0.102477 |

| exper | 0.034641 | 0.046674 |